|

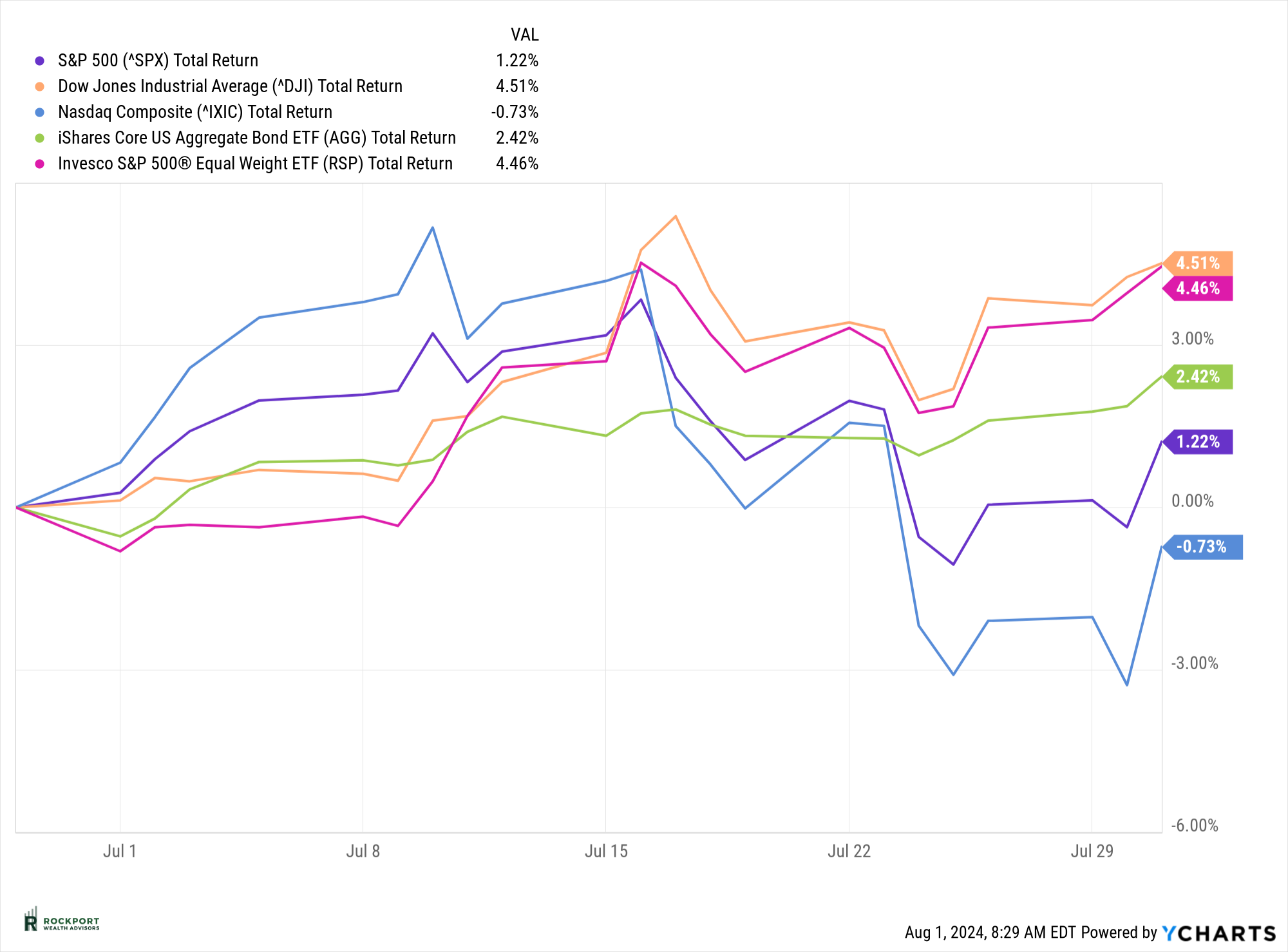

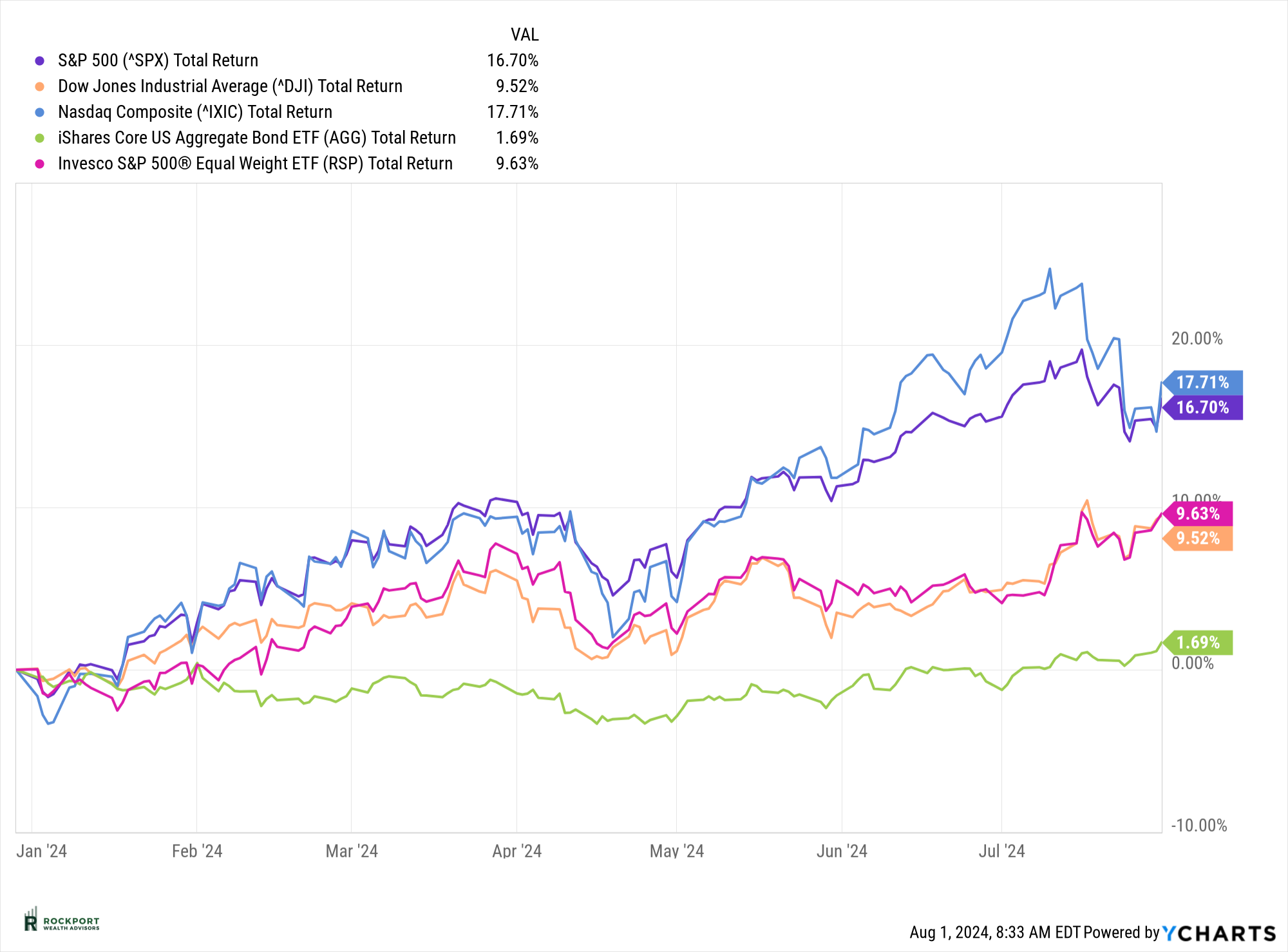

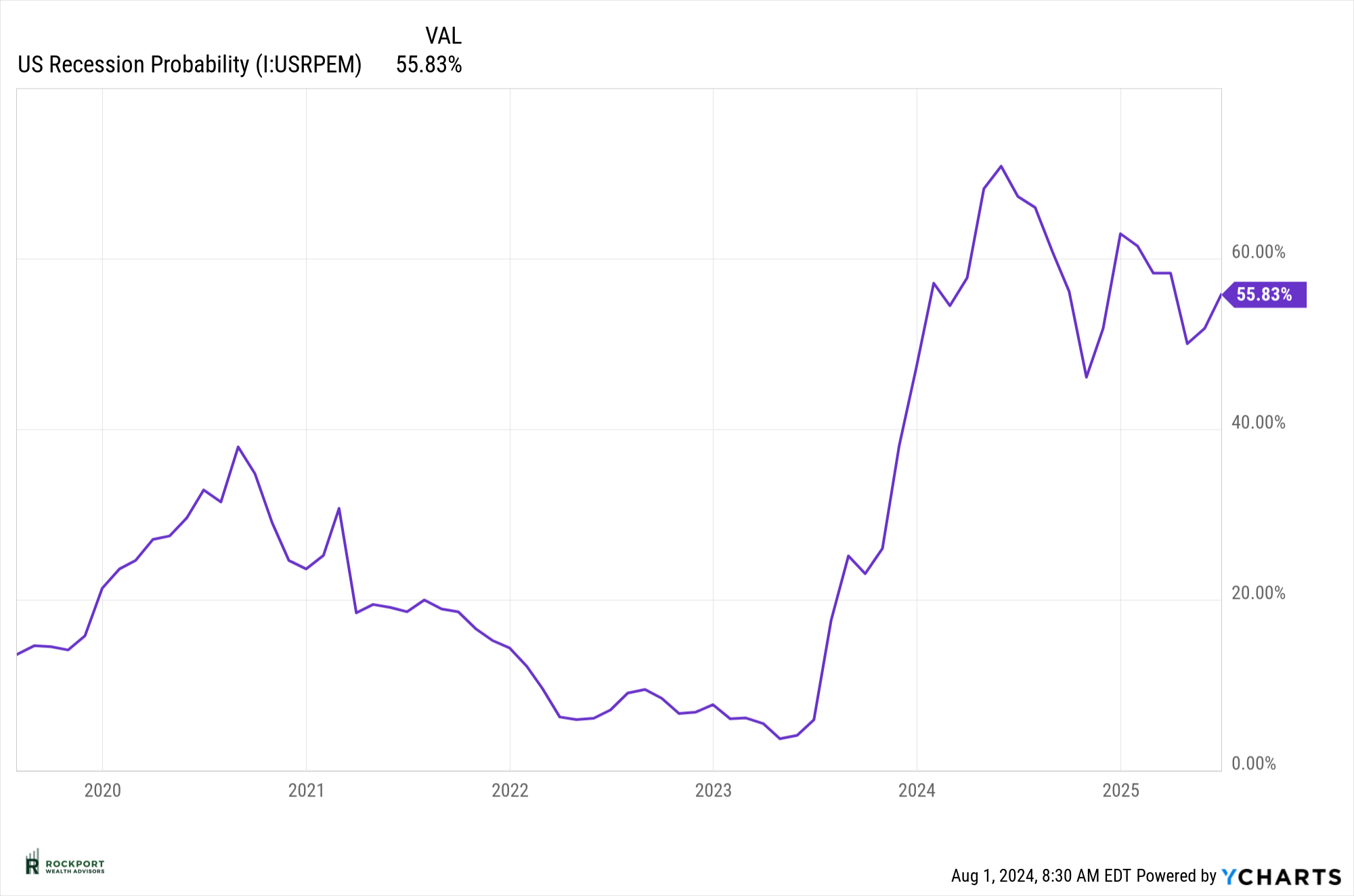

Markets & Economy July was an interesting month for the stock market. The S&P 500 index experienced a modest increase of 1.22%, bringing its year-to-date gain to 16.7%. In contrast, the S&P 500 Equal Weight Index rose by 4.46% for the month, resulting in a year-to-date return of 9.63%. This shift indicates a broadening of market gains beyond the high-tech large-cap growth names to other sectors, a welcome trend signaling healthy broad market participation. However, the month was not without volatility, particularly towards the end. On July 23rd, we witnessed the first day with a decline of over 2% this year, and the first such day since February 2023. This extended period without significant drops is unusual. As a result, it’s reasonable to expect more noticeable intra-day and weekly swings going forward. Despite these fluctuations, it’s crucial to remain composed and not be swayed by sensational media coverage or unqualified opinions on social media. Limiting or eliminating exposure to financial news can be beneficial during such times.

|

|

|

|

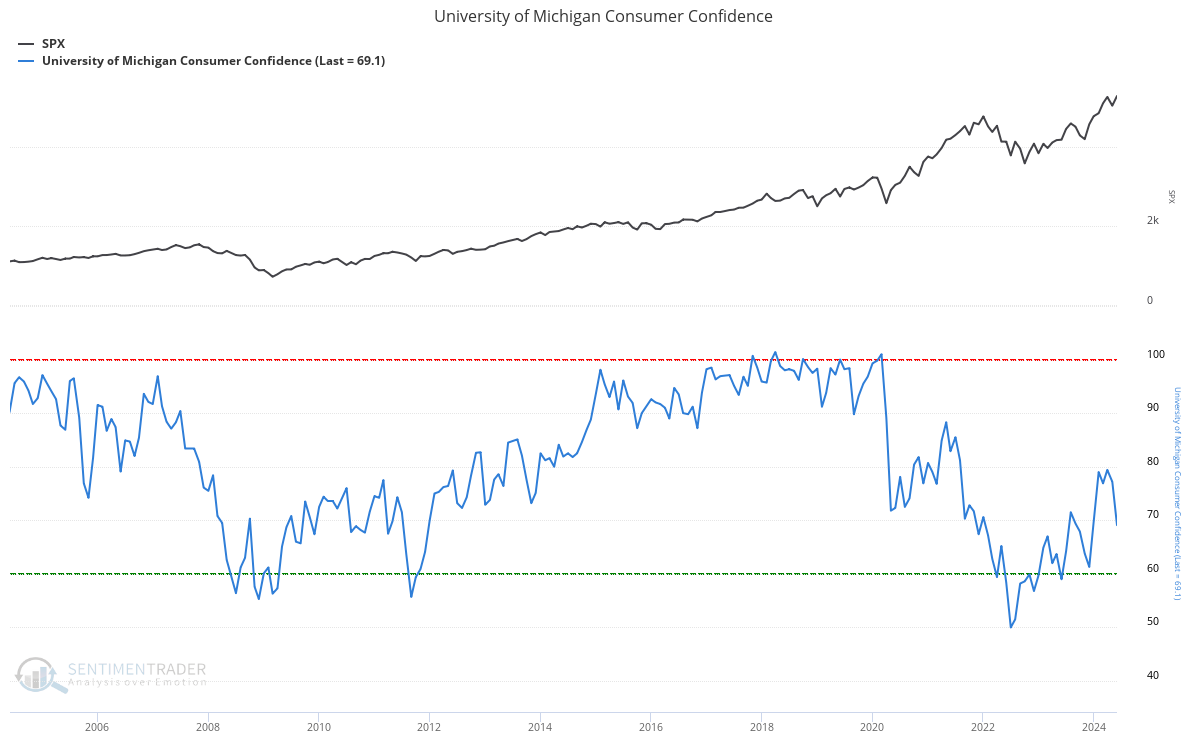

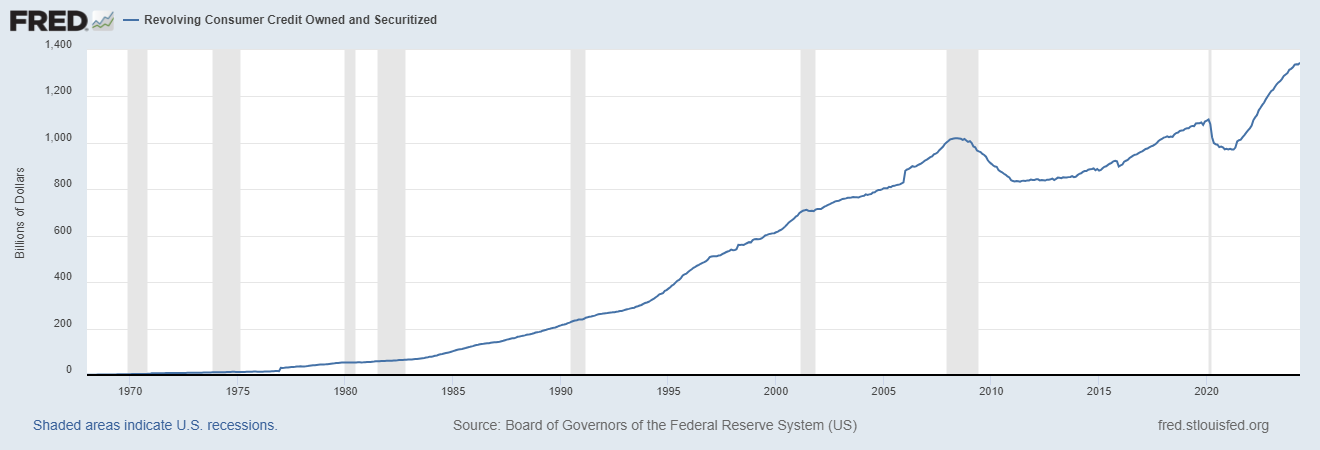

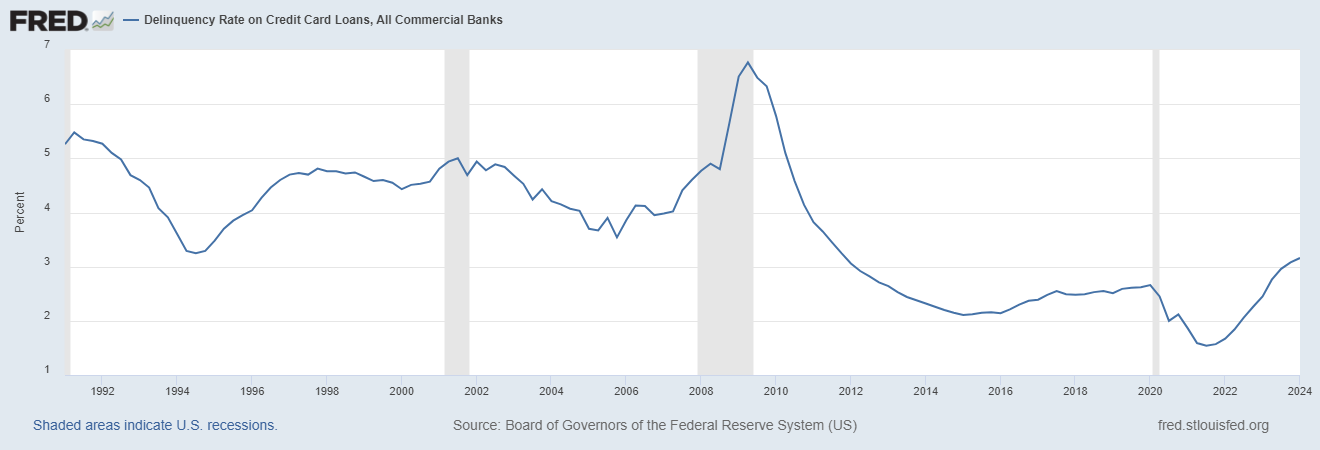

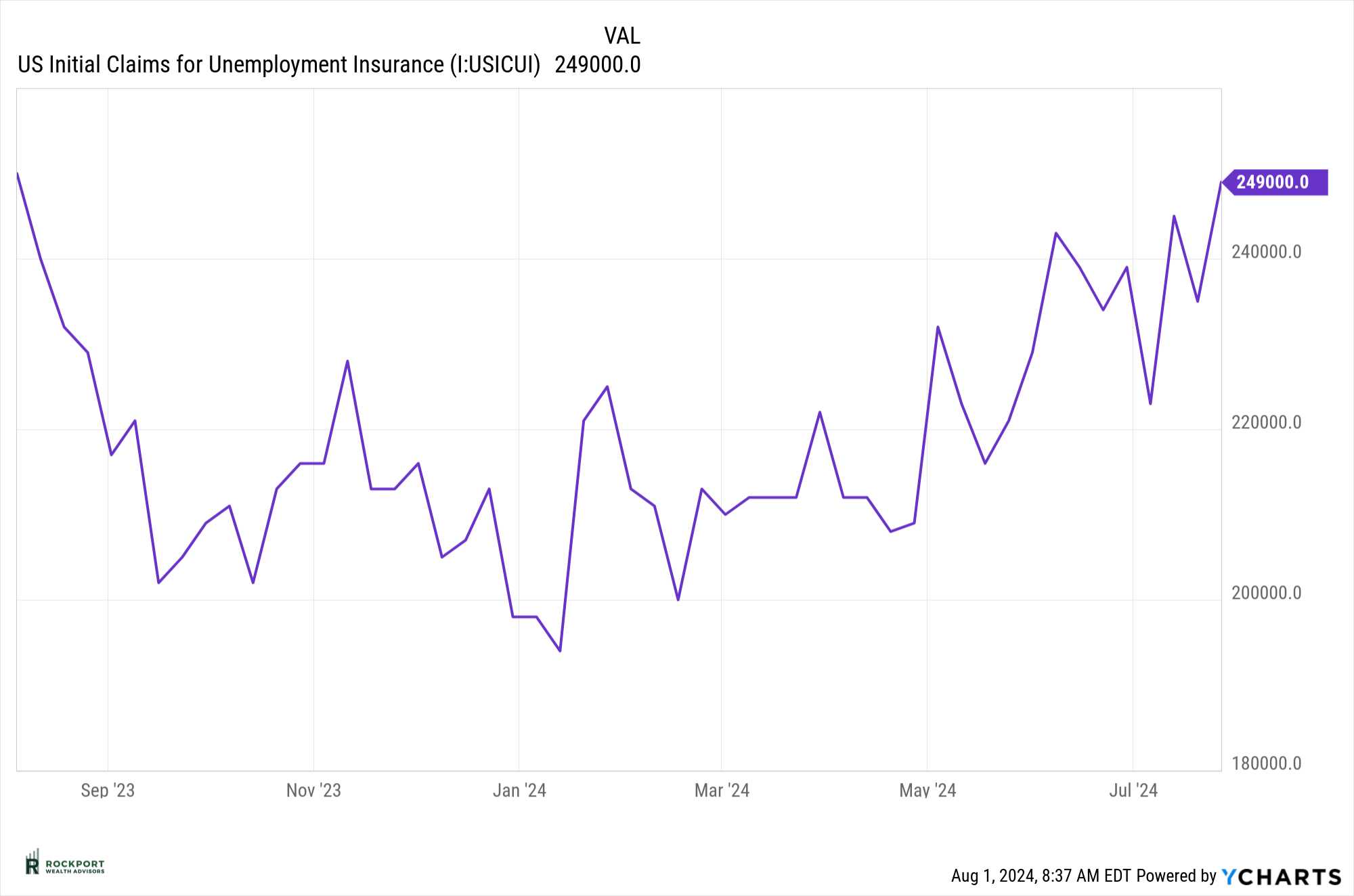

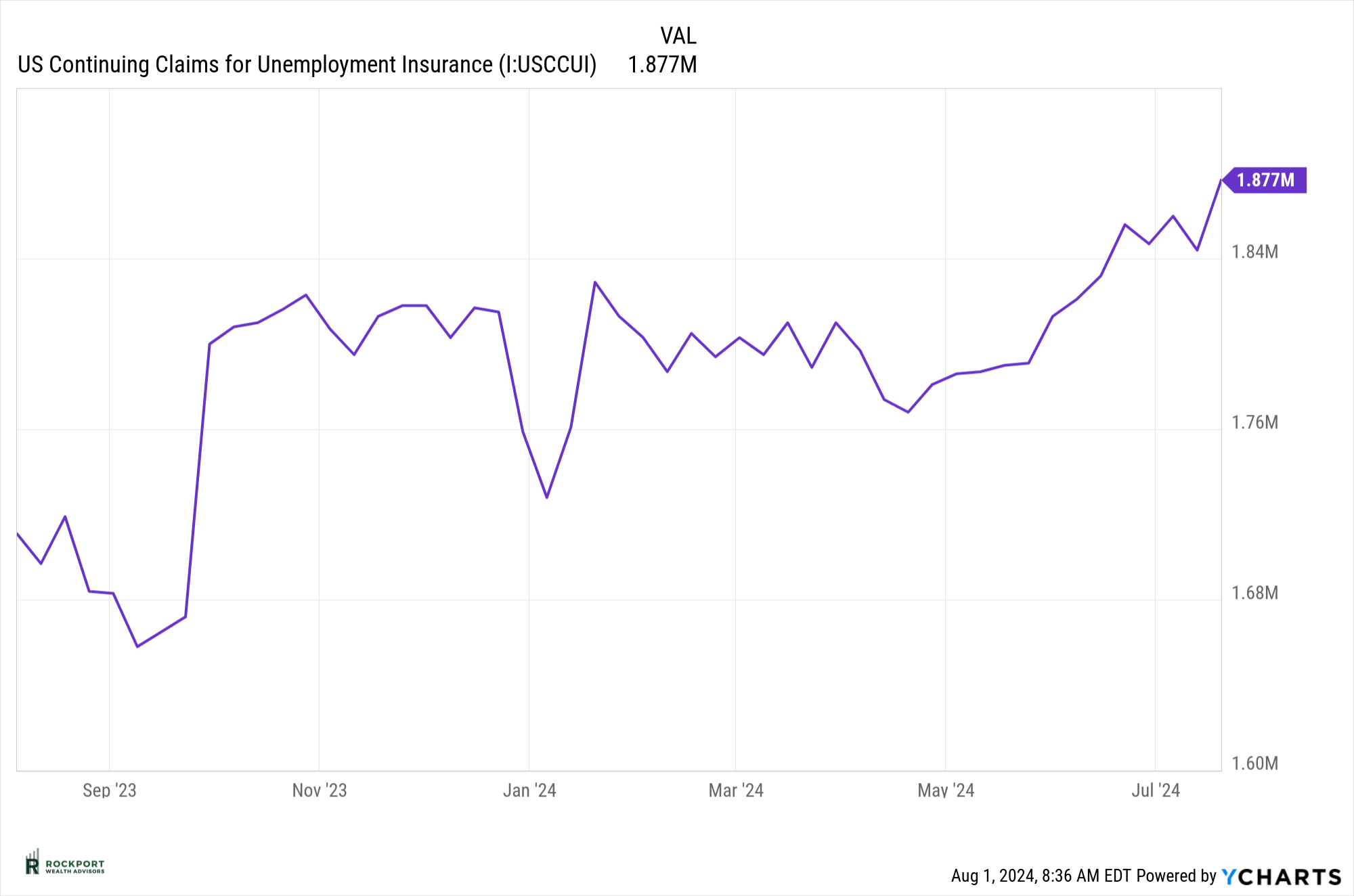

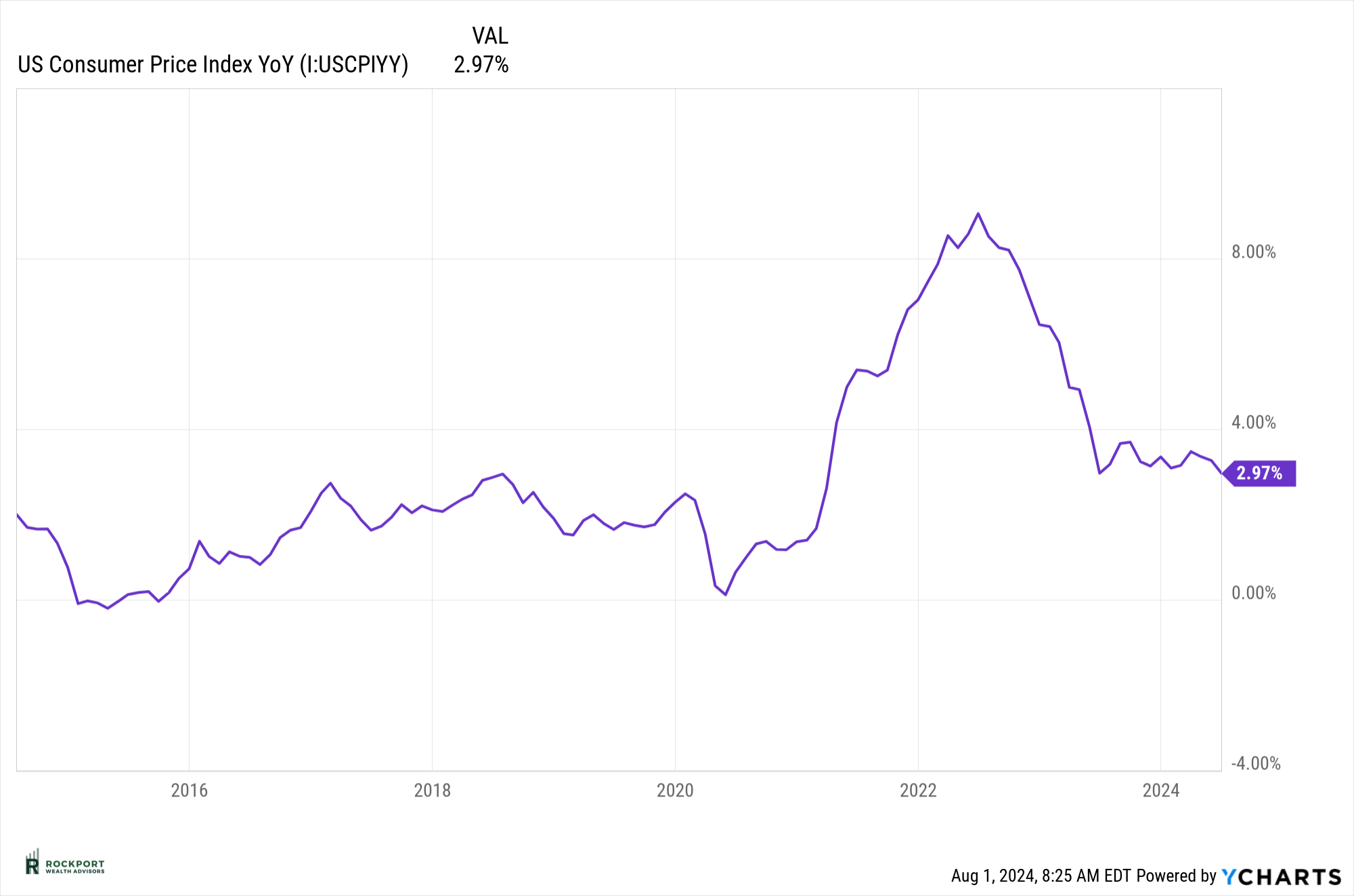

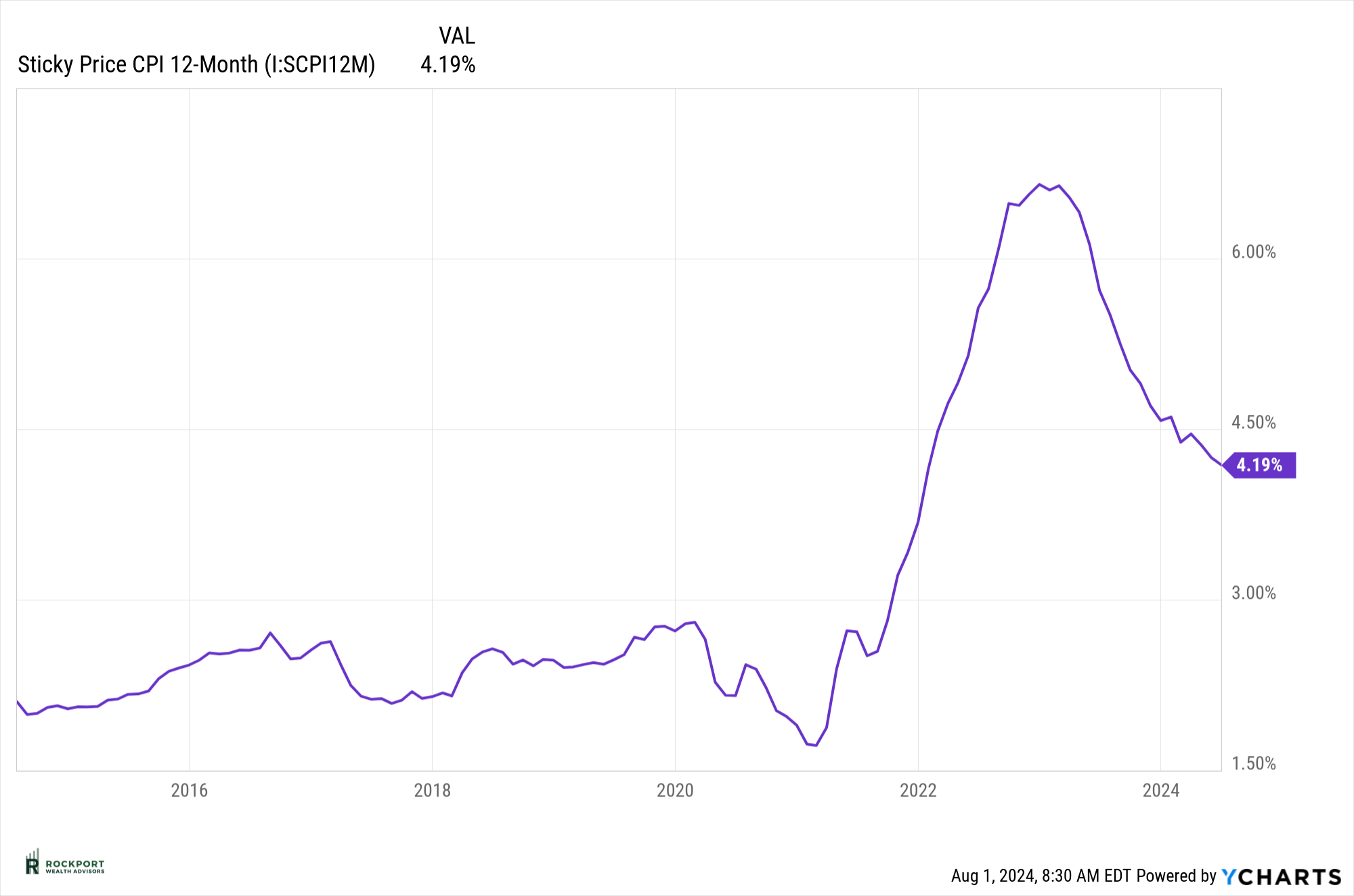

As we’ve highlighted many times, consumer strength is crucial in avoiding recessions. Currently, consumers are showing signs of slowing down and, in some cases, stress. Credit card balances remain at all-time highs, and default rates on these cards and other loans are at their highest level since late 2011. This will be a key area to monitor in the coming months. There is some good news on the inflation front: the Consumer Price Index (CPI) has dropped below 3% for the first time since 2021. This is a positive development, and we hope that consumer prices will continue to moderate in the coming months, especially as commodity prices have also declined. After more than two years of frequently discussing inflation, we will make this our final mention for now. We will continue to monitor this data internally, and if inflation shows signs of rising again, we will revisit the topic with updated charts. For now, we are putting this issue to rest, hopefully for an extended period. |

|

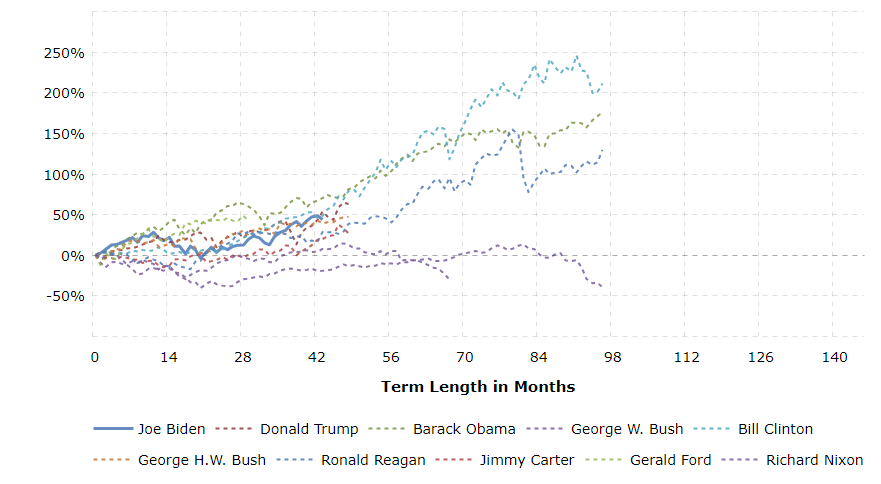

Lastly, with this being an election year there are a lot of questions. One common phrase is that if XYZ person gets elected the markets are going to tank. As you can see in the chart below, the stock market has had success under both parties and a long line of presidents. The only two presidents in modern times that had the stock market fall during their terms were Richard Nixon and George W Bush. So, let’s not assume a given outcome in the election will dictate future investment or that this time is different.

|

|