Happy Spring (Almost!) We hope this newsletter finds everyone happy and healthy.

***** We Are All Moved In *****

Thank you for your patience over the past couple of weeks as we worked to get settled in our new home.

J Arnold Wealth Management

7227 Glenwood Avenue

Youngstown, OH 44512

Jon Arnold’s View Point

The recent pullback in the growth sector, particularly technology, has been significant over the past two months. However, this development comes as no surprise—it’s simply part of the market cycle. The S&P 500 and Nasdaq delivered double-digit returns in 2023 and 2024, an unusually strong performance given the inflationary environment.

On a positive note, last year we proactively shifted most of our clients into balanced or more conservative portfolios where appropriate. This strategic move is now positioning our growth-oriented investors to re-enter the market at more reasonable valuations. While we may have been ahead of the curve, as I’ve emphasized in previous newsletters there is no timing the market.

One of the principles I emphasize in investing is maintaining control over Time, Emotion, and Discipline—or as I like to call it, TED. These three factors are critical to long-term success. Staying disciplined was particularly challenging last year as the S&P 500 and Nasdaq continued reaching new highs. However, both my research and instincts pointed to an unsustainable run, setting the stage for a potential correction.

I’m pleased to report that our portfolio positioning has prepared us well for the current market environment. It’s important to remember that risk is a matter of perspective. The majority of our clients are over the age of 55, which means they are in the retirement red zone—the crucial 10-year window leading up to retirement. Given this stage of life, we had to ask ourselves: Could we justify allocating the majority of assets to high-risk investments, especially with elevated P/E ratios, rising inflation, and looming market uncertainty? The answer was clear—we could not.

I want to extend my gratitude to all our clients for your patience and trust. Your commitment to a disciplined approach has not only helped us avoid unnecessary risks but has also positioned you for long-term success. Great job, and thank you!

What’s Next?

I anticipate that there will be some short-term challenges ahead. Ongoing issues like fluctuating tariffs, international relations, political tensions, and various global events are all contributing to the current volatility. However, what isn’t as widely discussed is the increasing financial strain faced by many: record numbers of individuals are withdrawing funds prematurely from their 401(k)s to make ends meet, credit card debt is at all-time highs, foreclosures are rising, and car repossessions are also on the uptick.

There are three potential ways out of this inflationary environment:

- Interest rate increases

- A recession

- A Black Swan event (e.g., 9/11, the banking collapse, or COVID-19)

While none of these options are ideal, I believe we are overdue for a recession, and I anticipate that it may be on the horizon. Historically, interest rate hikes and Black Swan events have led to significant market downturns, while a recession—though painful—could be the necessary catalyst to reduce inflation.

I want to be transparent with you: I believe a recession is likely, and a volatile market could persist for the rest of the year. However, this presents an opportunity. Thanks to our defensive portfolio positioning, we’ve been able to minimize short-term declines. When the right buying opportunities arise, rest assured that Joe, Adam, and I will be ready to capitalize on the situation.

In closing, I couldn’t be more proud of the position we’re in today and how we’ve navigated the challenges of the past 15 unpredictable months. I encourage you to reach out, watch our webinars, or visit us at our new office when you have the opportunity. We are here to support you and, most importantly, to help you stay focused and on track to achieve your financial goals. Thank you once again for being such a valuable partner in this journey—we’re grateful to be working alongside you in securing your financial success.

|

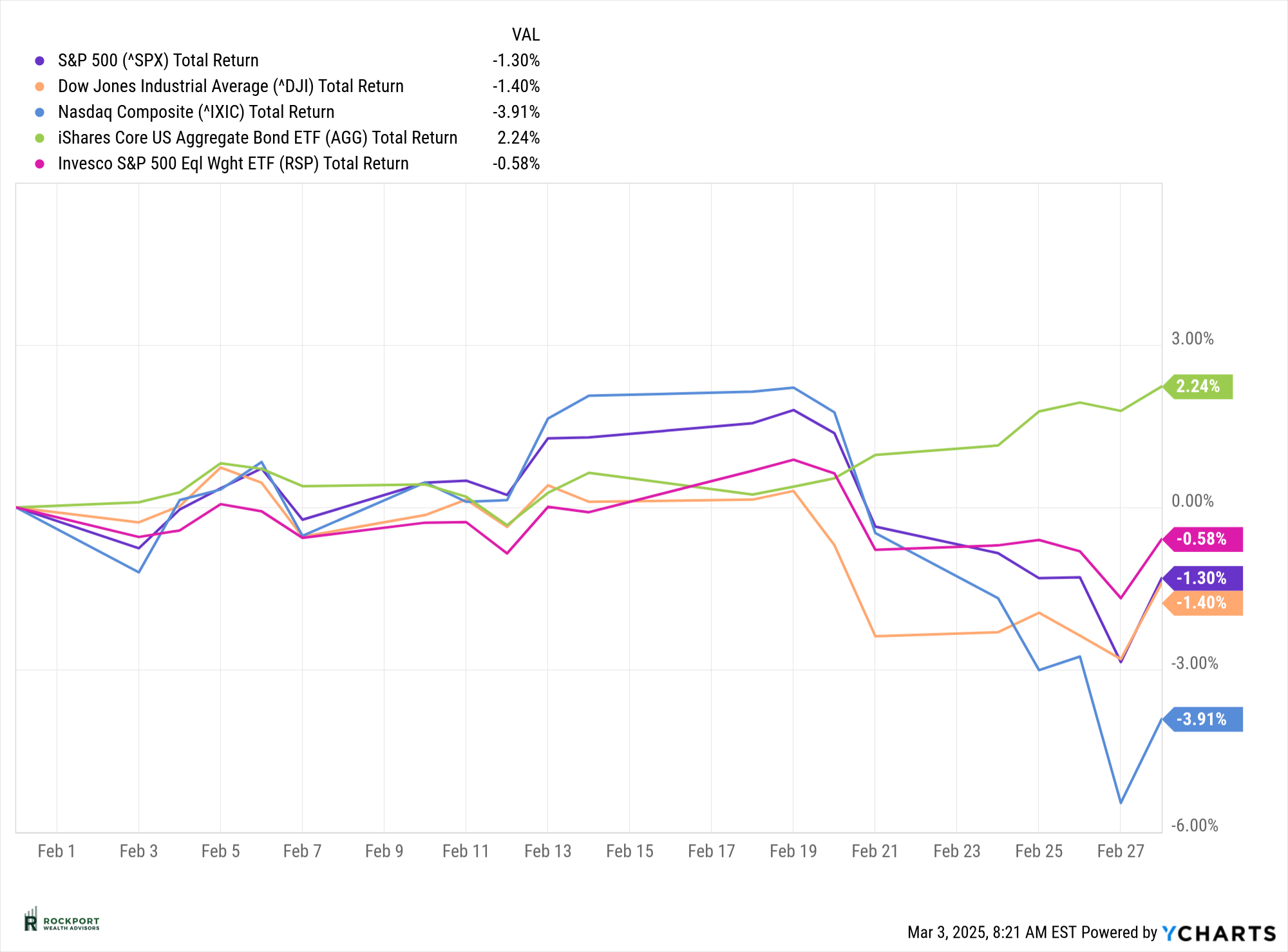

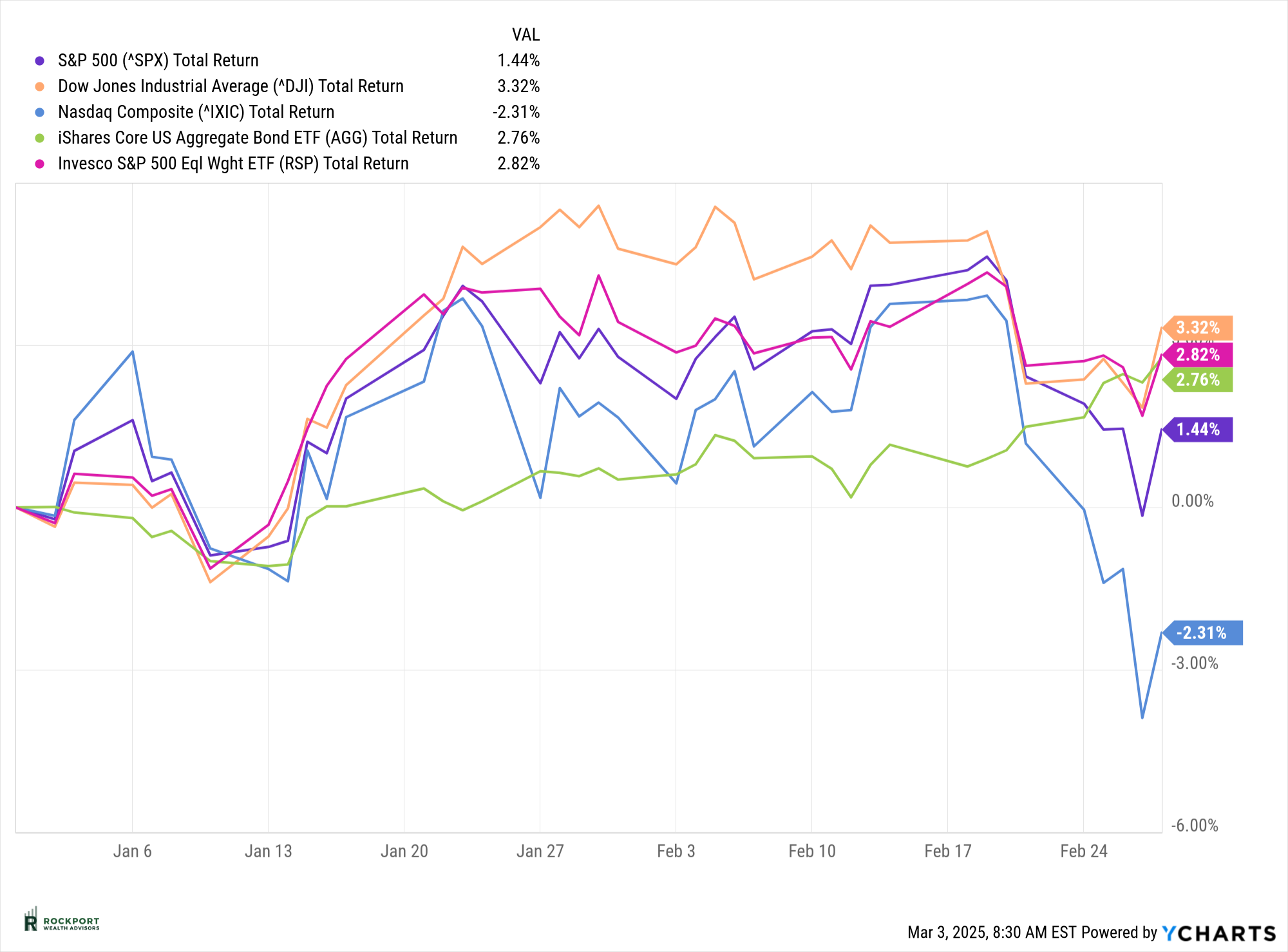

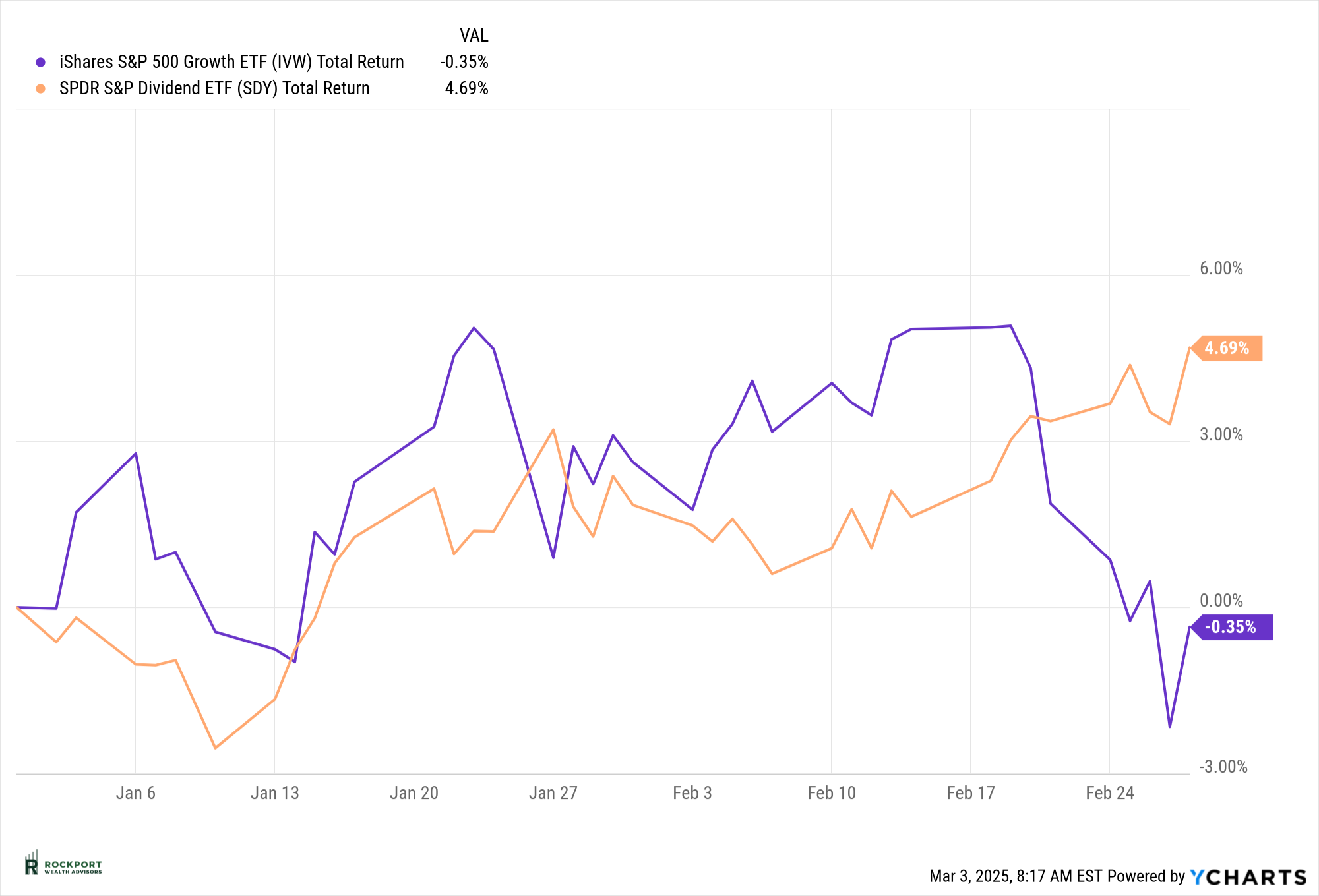

Markets & Economy As we mentioned in our last newsletter, we anticipated increased market volatility, and February proved that expectation correct. The S&P 500 declined by 1.3% for the month but remains in positive territory for the year, up 1.44% through the first two months of 2024. Other major indexes followed suit, with the NASDAQ experiencing a more significant decline of 3.91% in February. This index, which has been the hardest hit so far this year, is now down 2.31% year-to-date. A key driver of this weakness has been the performance of the “Magnificent 7” stocks (NVDA, GOOGL, MSFT, AAPL, AMZN, etc.), which have pulled back even more than the broader index. However, this isn’t entirely surprising, given that these stocks had seen some of the biggest gains in the preceding months and year. While market pullbacks can feel uncomfortable, it’s important to remember that they are a natural part of investing. Historically, 5% declines occur several times a year, and a 10% correction from recent highs happens about once per year. These dips, while normal, can still feel unsettling—but they are an expected part of long-term market cycles. Interestingly, the best performing areas of the market this year have been the equal-weight S&P 500, the Dow Jones Industrial Average, and bonds. Essentially, the investments that lagged in the previous year have led the way so far in 2024, signaling a broadening of market performance at the expense of high-valuation growth stocks. One final noteworthy trend: for the first time in quite a while, value stocks are outperforming growth stocks. It feels like ages since this has been the case, but so far in 2024, portfolio composition has played a significant role in returns. Investors with a heavier allocation to technology and growth stocks have underperformed those with greater exposure to value and dividend-paying stocks.

|

Several factors seem to be driving the short-term market volatility we’ve seen recently. Ongoing trade tariffs, uncertainty around economic growth, persistent inflation that complicates the Federal Reserve’s decision-making, and concerns about employment have all contributed to the market’s choppiness.

Let’s take a closer look at this issue. The current administration has implemented tariffs on multiple countries, raising concerns that inflation could worsen as a result. Adding to the uncertainty, these tariffs have been announced, reversed, and then delayed—sometimes within days—creating a lack of clear direction. This inconsistency in messaging has been unsettling for the stock market, as uncertainty is one of the biggest challenges for investors. Unfortunately, this remains a wait-and-see situation, and we should expect this storyline to continue playing out for some time.

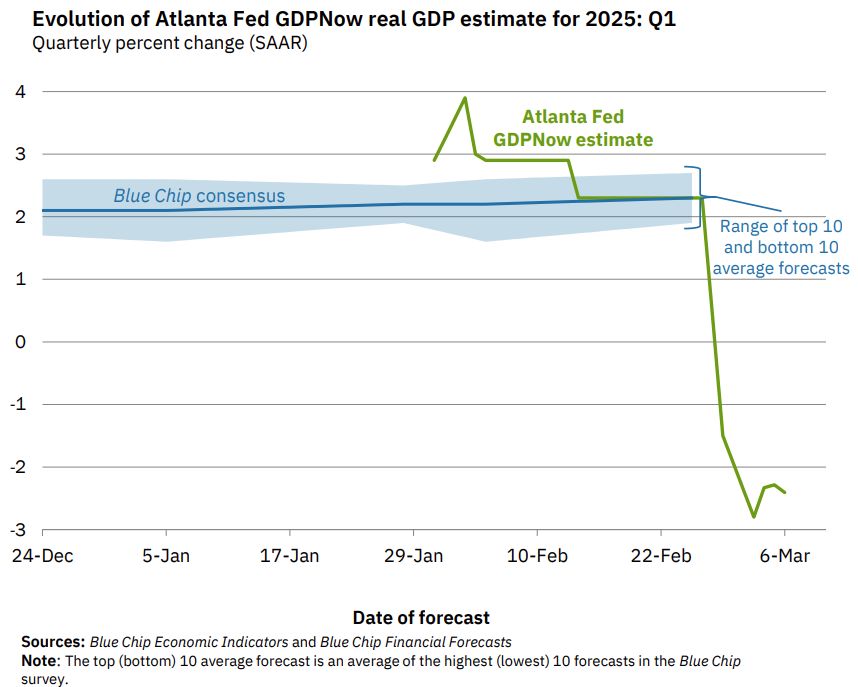

The strength of economic growth is now in question. One key measure of growth, Gross Domestic Product (GDP), is closely watched by economists and investors alike. As shown in the chart below, the Atlanta Fed’s latest GDP Now forecast is currently projecting negative growth for the first quarter of this year (green line). While this is just one of many forecasts and should not be viewed in isolation, it is noteworthy as the first negative projection we’ve seen in some time. This will be an important trend to monitor closely.

It’s also worth remembering that a technical recession is defined as two consecutive quarters of negative GDP growth. While we’re not there yet, this is a development that warrants attention in the months ahead.

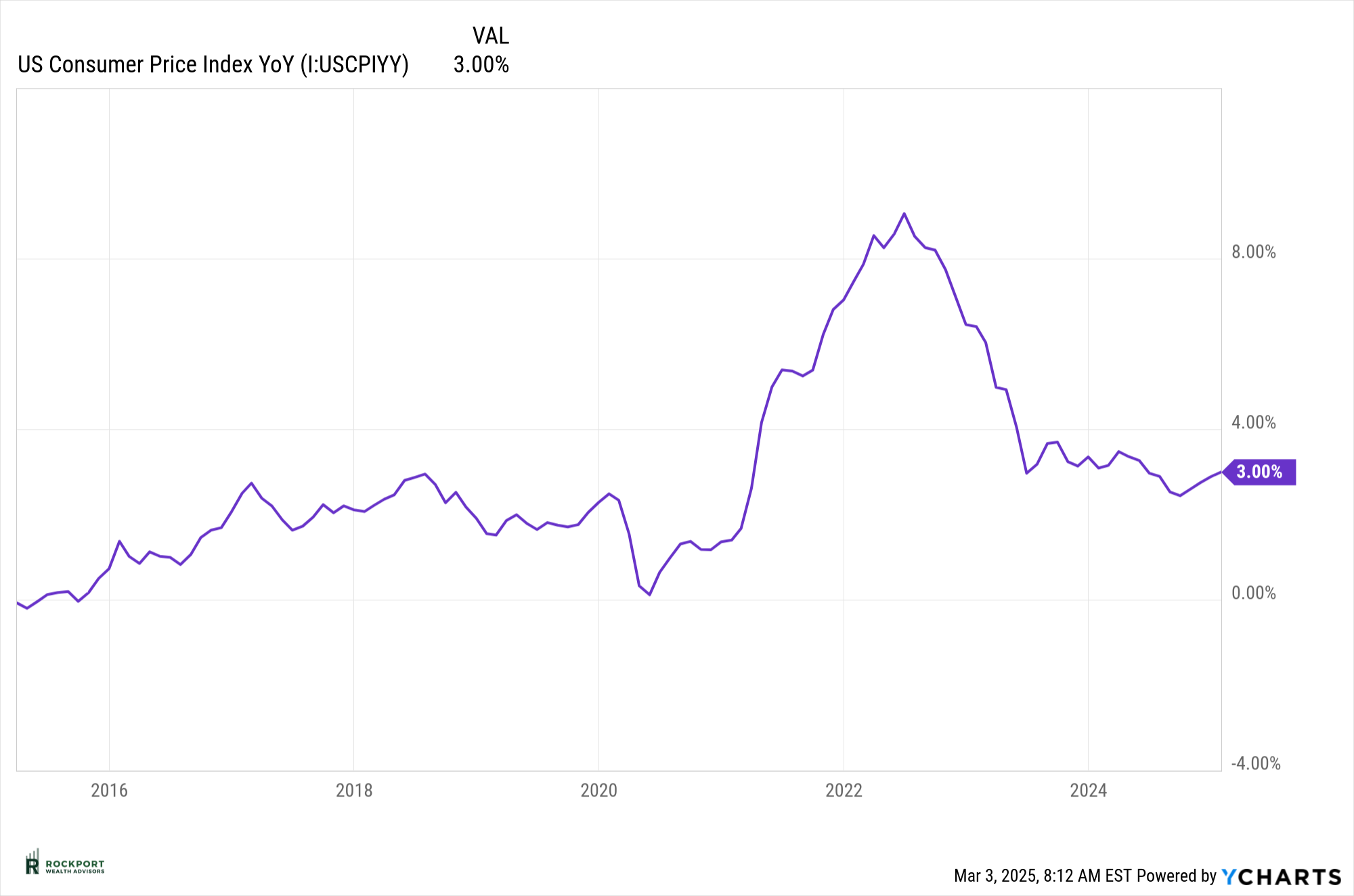

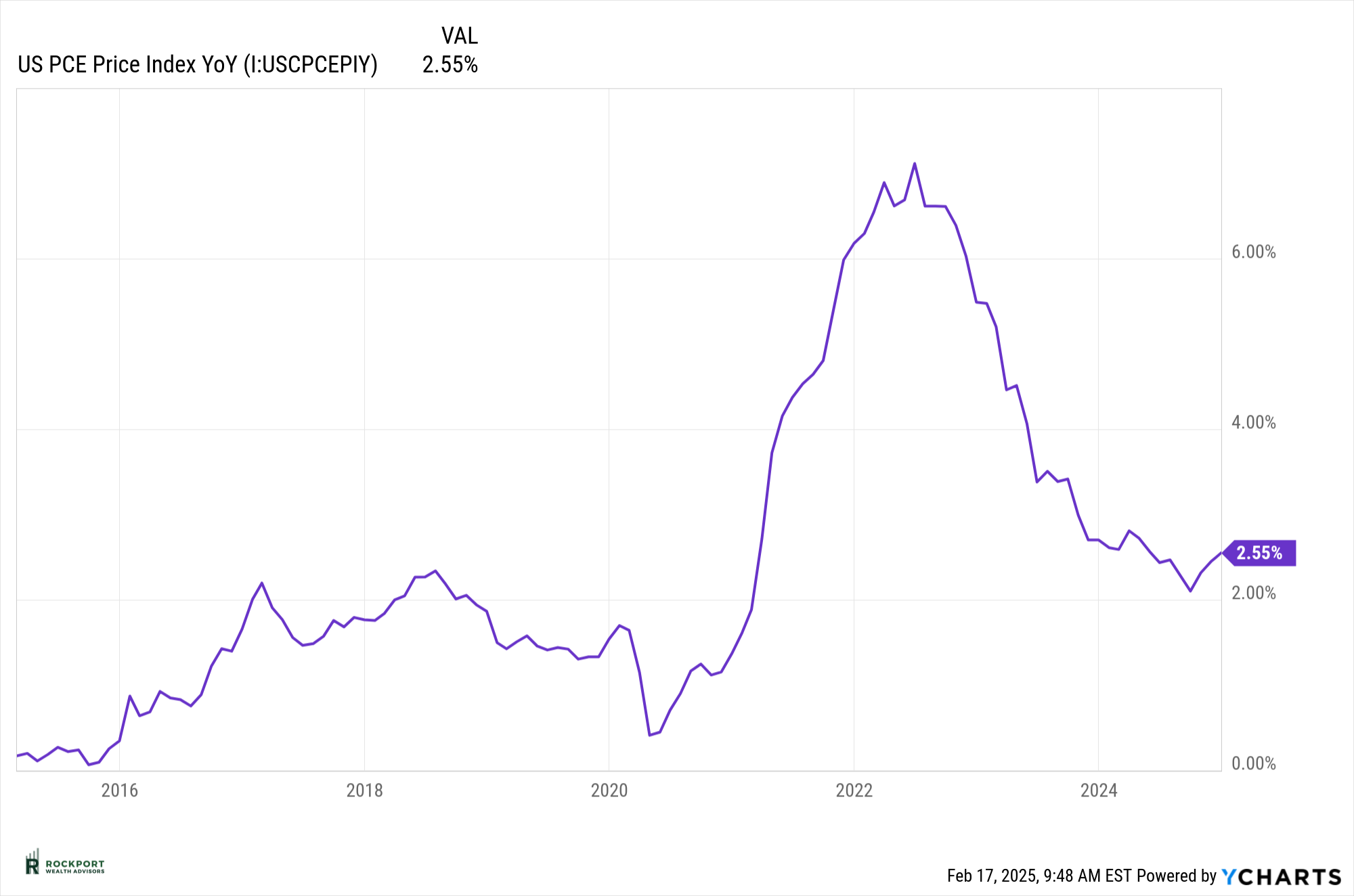

Inflation has remained a key concern for some time now, as we’ve discussed in previous newsletters. As of January, inflation continued to rise, with both the Consumer Price Index (CPI) and Personal Consumption Expenditures (PCE) index maintaining their upward trend since September. While this persistence is not ideal, there are emerging signs that inflation may be cooling.

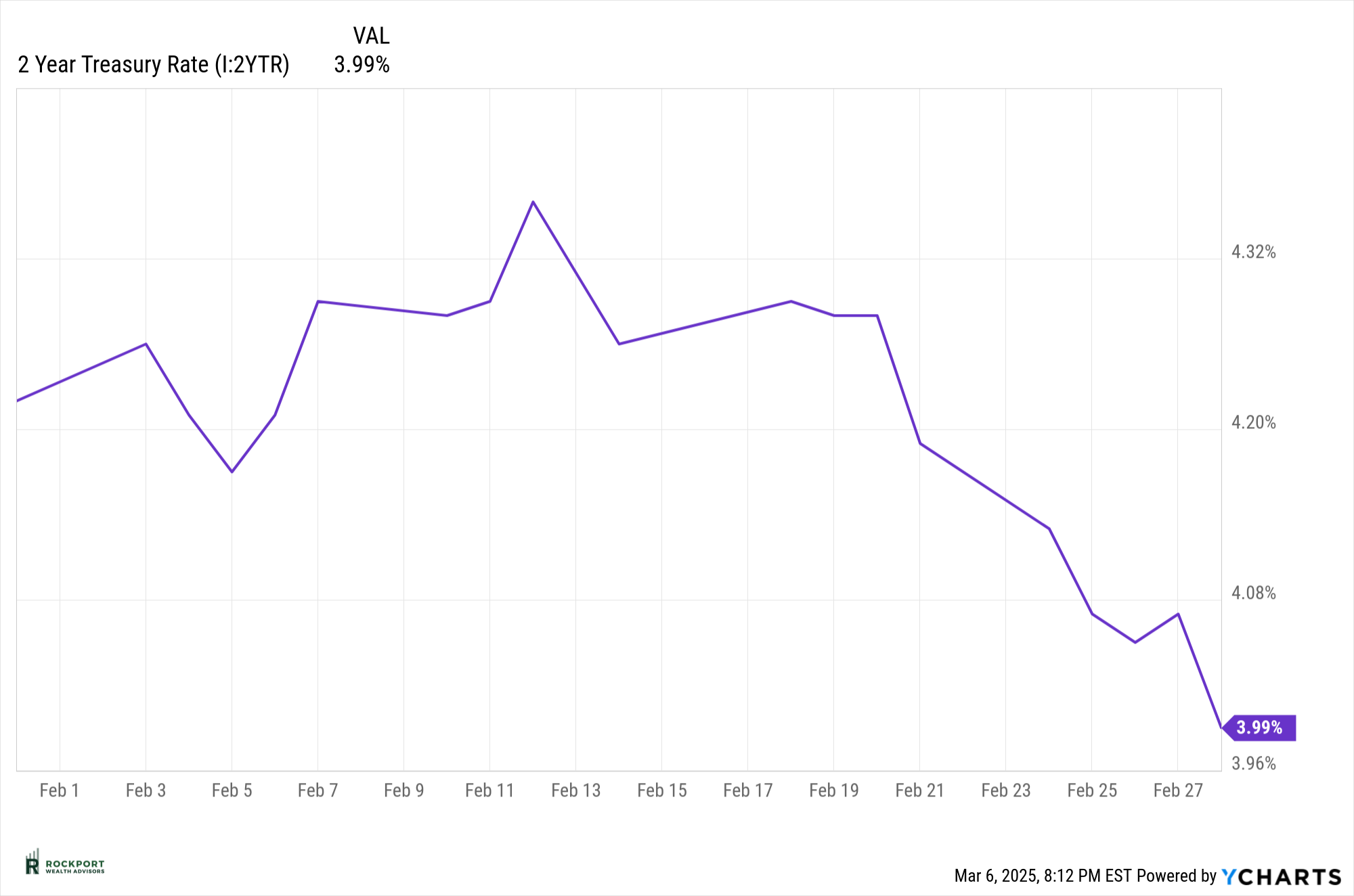

One potential indicator is the recent movement in the 2-year Treasury yield. Since mid-February, the yield has fallen notably from 4.36% to 3.99%. This decline is significant, as the 2-year yield is now well below the Federal Funds rate of 4.50%, which could suggest that inflationary pressures may ease in the months ahead. Historically, the 2-year Treasury yield has been a strong indicator of where the Federal Reserve may be headed with interest rates.

Just a month ago, market expectations suggested little to no room for rate cuts in 2024. Now, with this shift, forecasts have adjusted to potentially two to three rate cuts this year. While nothing is certain, we will be watching this closely in the coming months to see how the Fed responds to these evolving economic conditions.

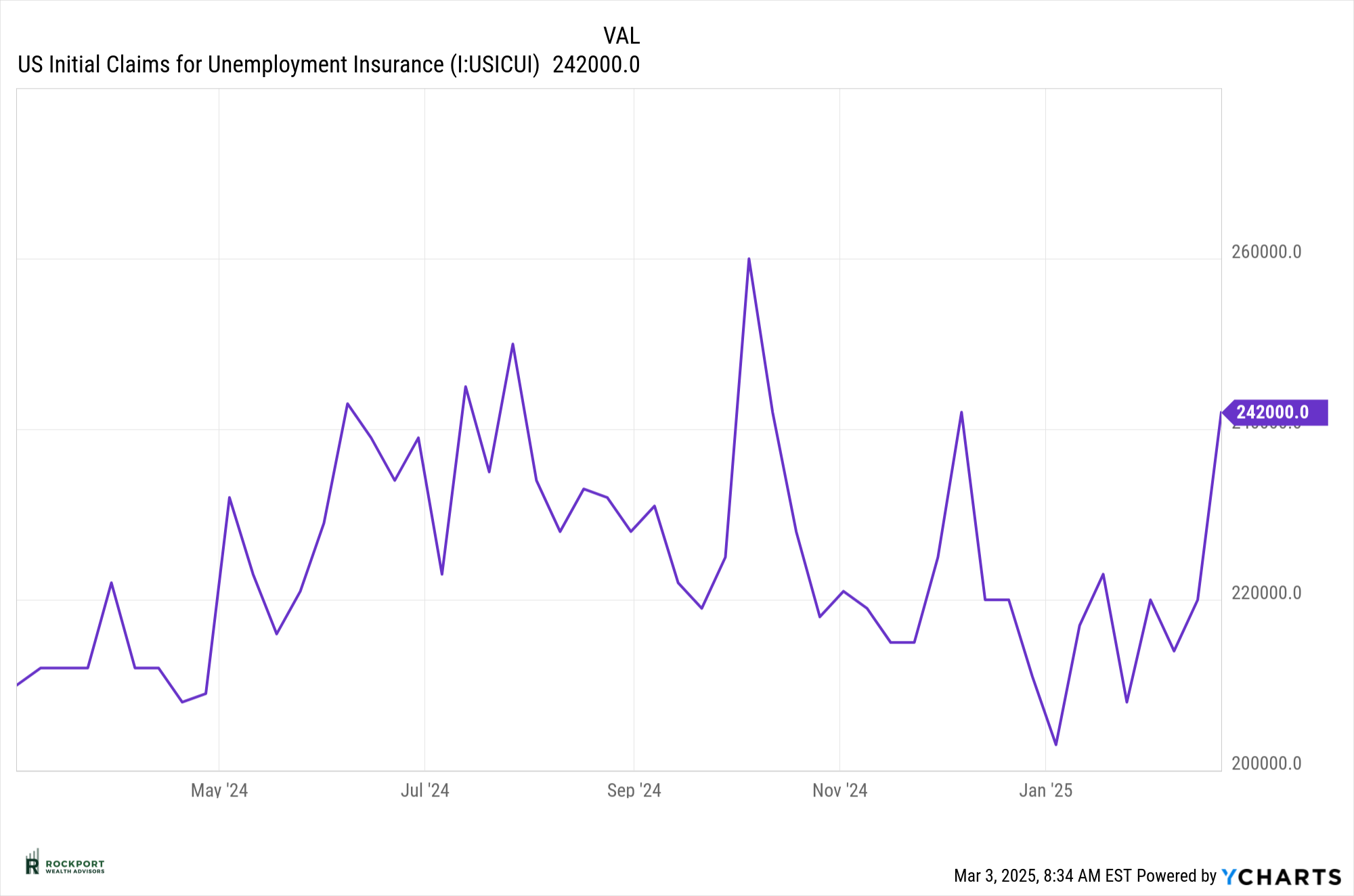

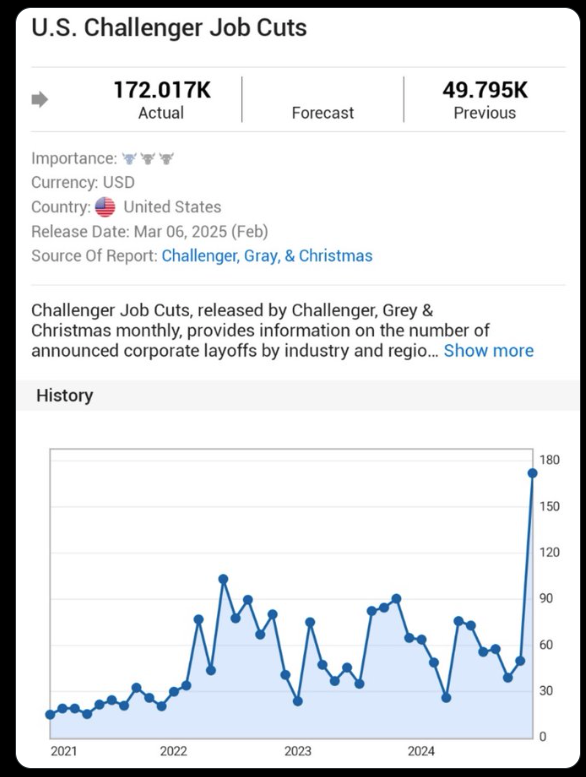

Employment may become a key concern in the months ahead. While continuing unemployment claims have remained stable for now, initial jobless claims are beginning to trend higher. Additionally, as shown in the chart below from Challenger, Gray & Christmas, job cut announcements have spiked, signaling potential trouble ahead for the labor market.

With widespread layoffs already announced across various industries—and additional cuts expected at the government level—unemployment could be on the rise. This will be an important trend to monitor as we assess the broader economic outlook.

As we move forward in 2025, the year is shaping up to be an eventful one. With headlines dominated by tariffs, foreign relations, and economic concerns, the media’s tendency to amplify uncertainty can make it challenging to separate noise from reality.

One key question remains: Will the long-anticipated recession that never materialized in 2024 finally arrive, or will the economy continue to defy expectations? As the government embarks on the gradual unwinding of the unprecedented fiscal stimulus that has fueled the U.S. economy over the past 8-10 years, we are likely to experience additional volatility. Much like a child coming down from a sugar high.

While challenges lie ahead, staying focused on long-term fundamentals rather than short-term headlines will be essential. We’ll continue to monitor these developments closely and provide guidance along the way.

As always, if you have any questions on anything we have talked about here or anything else that is on your mind, please feel free to reach out.